All contributors to the 2024-25 FAFSA are required to provide consent to retrieve and disclose Federal Tax Information (FTI) from the IRS to the Department of Education. Once consent is provided, the IRS automatically sends FTI, eliminating manual entry of income and tax information for contributors that filed 2022 US federal taxes.

If any contributor to the student’s FAFSA does not provide consent, the student will not be eligible for federal student aid, including grants, loans and work-study. Consent is required by every contributor regardless of their US federal tax filing status.

Who is a contributor to the FAFSA?

For dependent students, contributors are:

- The student

- The student’s biological or adoptive parent or parents who are completing the FAFSA.

- If the parents are married and file taxes “Married Filing Jointly”, then only one parent is required to be a contributor and can complete the entire FAFSA Parent Section. In this case, only the parent contributing must provide consent.

- If the parents are married and file taxes “Married Filing Separately”, then both parents are required to be contributors. Each parent contributor must consent for their FTI to be shared.

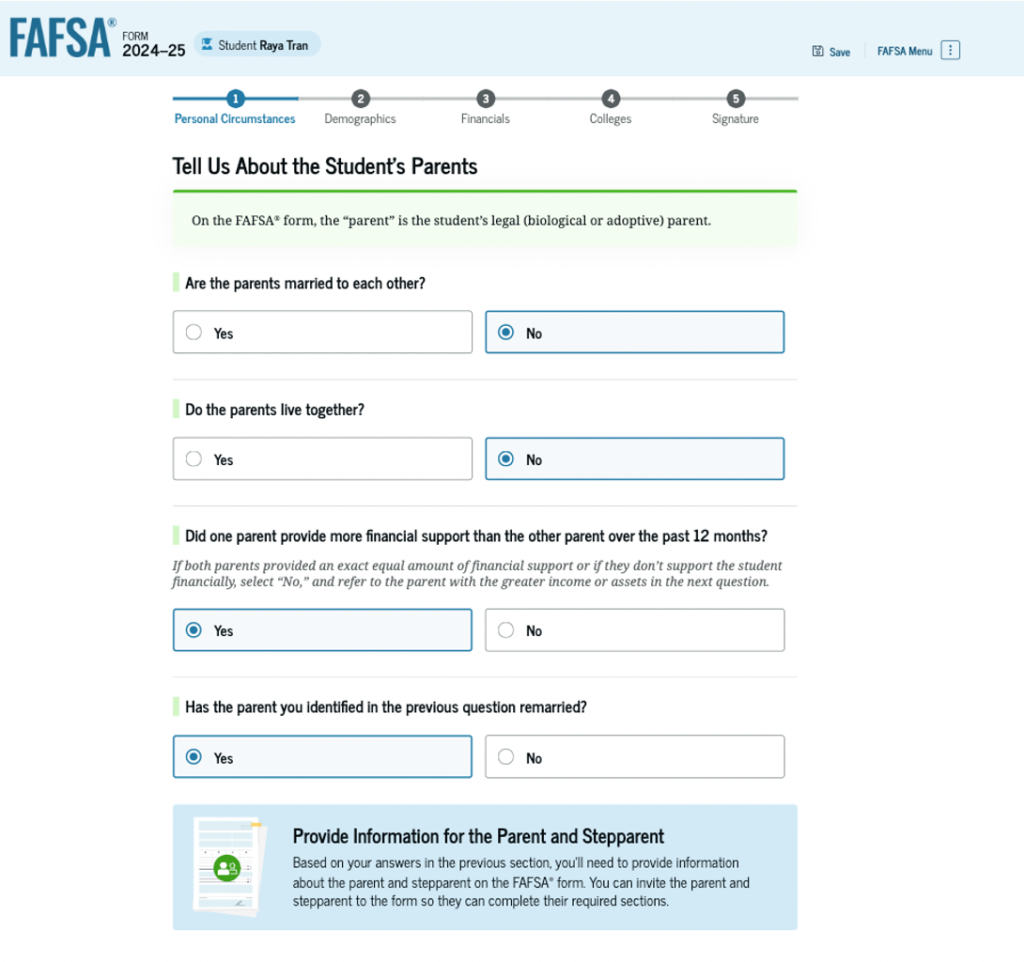

- If the parent is single, separated or divorced from the other biological or adoptive parent, then only the parent that provided the greater financial support in the 12 months prior to application would be a contributor and would need to consent. However, if that parent contributor is remarried, their spouse would be included in the parent FAFSA section. See more information, see New rules for single, separated or divorced parents.

What if the student or parent doesn’t file U.S. federal taxes or files taxes in another country?

Even in these cases, every contributor must provide consent. If no FTI is found, then the parent or student manually enters income and tax information.

What are other reasons why no Federal Tax Information (FTI) would be shared?

Every contributor must consent, but here are other reasons FTI would not be shared. In each of these cases, the contributor has to manually enter income and tax information.

- Non-tax filers. These individuals aren’t required to file taxes because they are below the income requirements for mandatory tax filing. The most common case is a student who did not earned income in 2022 or didn’t earn enough to file taxes. Parents may also qualify as a non-filer.

- Foreign tax filers. These contributors follow prompts to enter the equivalent information, converted to US dollars, from their home country’s tax forms.

- Late tax filers. If a contributor has not yet filed taxes, they must provide consent and manually enter estimates. The FAFSA system will continue to contact the IRS to check for a filed tax form after the FAFSA submission. If that FTI is later found, it will replace the manually entered information. Ultimately, if a parent is required to file taxes, the college’s financial aid administrator will be required to collect the tax forms before aid is dispersed to the student.

- Victims of identity theft. In this case, the IRS may not share information. These contributors enter income and tax information manually.

- Recently divorced or separate parents who filed jointly with their ex-spouses in 2022. Because the 2022 “Married Filing Jointly” tax return has income and tax information from both parents, but only the custodial parent is required to contribute, the FAFSA will not use the FTI shared by the IRS. Instead, that parent contributor manually enters separated income and tax information to accurately reflect earnings for that individual parent.

If the contributor filed taxes, is there still an option to manually enter income and tax information?

If the contributor filed US tax return and provides the required consent, the answer is no. The cases for manual entry of income and tax information are listed above.

Can a contributor see the Federal Tax Information (FTI) that has been shared?

No. Because FTI is considered confidential, it will not appear in the application or the FAFSA Submission Summary. Even the questions associated with that information will not be shown to the contributor.

What if a contributor doesn’t provide consent?

If any contributor to the student’s FAFSA doesn’t provide consent, the student will not be eligible for federal student aid, including grants, loans and work-study. Consent is required by every contributor regardless of their US federal tax filing status.

Can a contributor who declined consent initially, go back and provide consent later?

Yes. Any contributor that previously declined consent can log into their section of the FAFSA and provide consent. Once consent is provided and FTI is shared, manually entered income and tax information will be replaced.